Commercial Energy Audit Report Breakdown. What You Actually Receive

When people ask for an energy audit, what they usually want is clarity.

Not a technical document.

Not 80 pages of engineering commentary.

They want to know:

Where is the energy going

What is it costing

What can be fixed

What it will cost to fix

What the return looks like

What should be done first

This is what a properly structured energy audit report delivers.

Under AS/NZS 3598, both Type 2 and Type 3 audits follow a defined structure. The depth changes, but the purpose does not. The report must support decisions.

Below is what decision makers actually use from a commercial energy audit report

Executive Summary. The Page That Gets Read First

For a CFO or Asset Manager, this is the most important section.

A strong executive summary includes:

Total annual energy consumption by fuel

Total annual energy cost

Site emissions baseline

Number of opportunities identified

Total potential savings

Capital required

Simple payback and high-level ROI

In many cases, this summary is what goes to the board.

If this page is unclear, the rest of the report will not be used.

Energy Baseline and Load Profile Analysis

This section explains how the site actually consumes energy.

It typically includes:

12 to 24 months of electricity and gas data

Seasonal demand variation

Peak demand drivers

After-hours base load

Weekend and shutdown performance

On real sites, this is where operational issues become visible. Common findings include:

HVAC running outside required hours

Compressed air left online during shutdown

Simultaneous heating and cooling

Excessive base load in office buildings

Demand spikes caused by plant sequencing

This is the point where Facility Managers recognise their site in the data.

System Breakdown by Major Load

Under AS/NZS 3598, the report must identify significant energy users.

This section usually breaks energy into:

HVAC plant

Lighting

Process loads

Refrigeration

Compressed air

Pumps and fans

Hot water systems

In a Type 2 audit, this breakdown is based on site inspection, nameplate data, runtime assumptions, and interval data.

In a Type 3 audit, this may include deeper modelling, metering validation, and engineering calculations.

For Operations Managers, this is where reliability risk often becomes clear. Ageing chillers, oversized compressors, or inefficient boilers show up not just as cost issues, but as operational exposure.

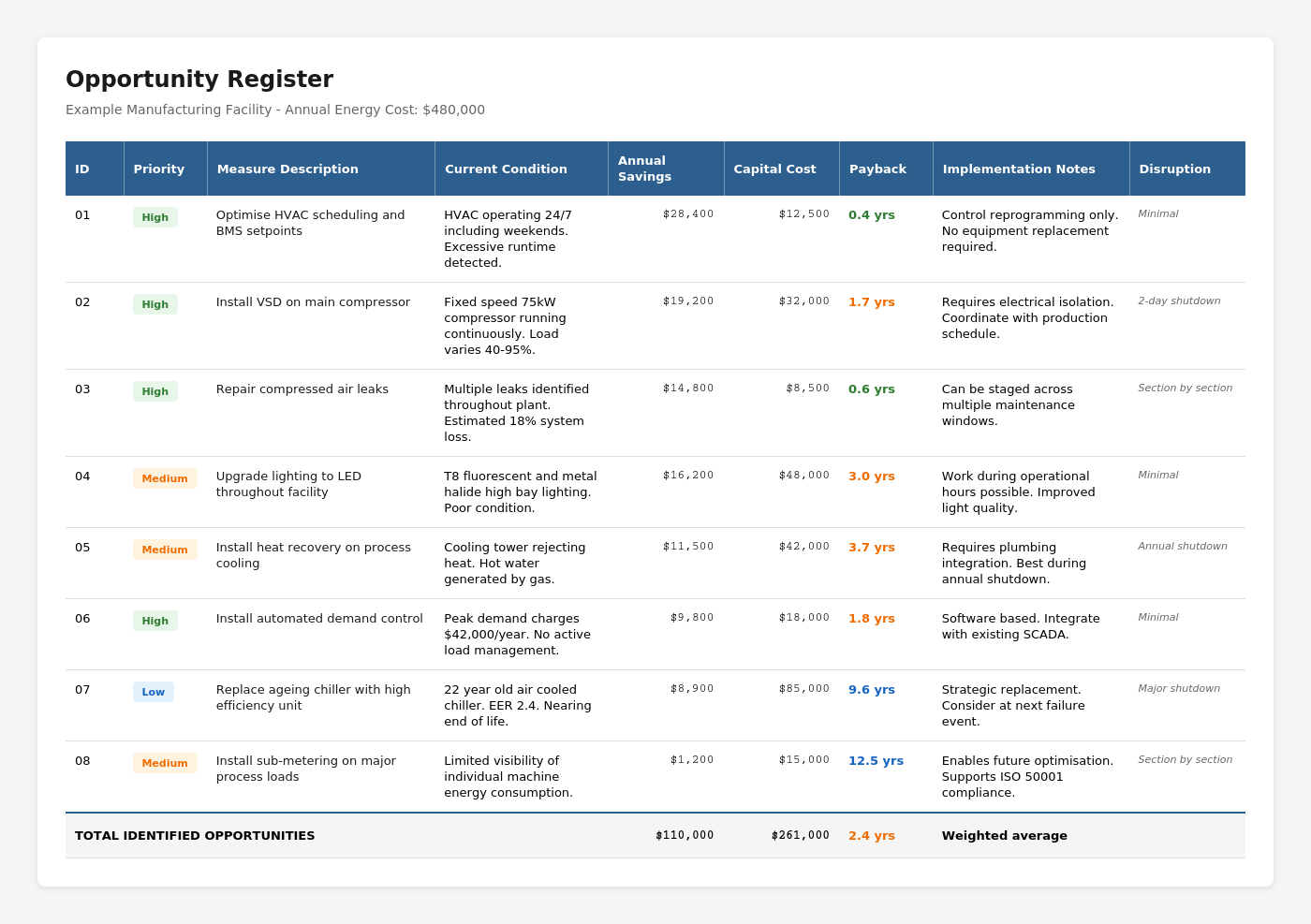

Energy Conservation Measures. The Most Used Section

This is the working tool.

A properly structured opportunity register includes:

Stronger financial analysis and more granular data-based review of key energy-consuming equipment.

This register becomes the internal action list.

Facility teams use it for planning shutdown work.

CFOs use it for budget forecasting.

Asset Managers use it for capital prioritisation.

Without this structured table, the report becomes reference material rather than a decision tool.

Capital Prioritisation and Staging

Decision makers rarely implement everything at once.

A good audit report separates measures into:

Low-cost operational improvements

Mid-range optimisation upgrades

Capital-intensive plant replacements

Capital-intensive plant replacements

Often presented as:

Short term. Under 2-year payback

Medium term. 2 to 5 years

Long term. Strategic asset replacement

This staged approach recognises real site constraints:

Budget cycles

Contractor availability

Shutdown windows

Procurement processes

Asset replacement timing

This is where the audit shifts from theory to implementation planning.

Financial Analysis. What Makes It Board Ready

Because this article references AS/NZS 3598, the financial treatment differs between Type 2 and Type 3 audits.

Type 2 audits generally provide:

Indicative capital cost estimates

Simple payback

High-level ROI

Type 3 audits go further, often including:

Discounted cash flow

Net Present Value

Internal Rate of Return

Sensitivity analysis

For typical clients, large commercial and industrial energy users, the blended approach works well.

Provide sufficient financial rigour to build confidence in decisions, but avoid excessive modelling that delays action.

Indicative Example

Indicative example based on a typical commercial audit scope:

Annual energy cost is approximately $480,000

Identified savings potential of approximately $110,000 per year

Required capital is approximately $320,000

Weighted average simple payback 2.9 years

Low-cost control improvements delivered:

12 per cent savings

Under 12-month payback

Capital upgrades focused on:

HVAC plant optimisation

Variable speed drives

Demand control

Heat pump hot water replacement

The key outcome was not just a list of savings.

It was a staged plan aligned to maintenance cycles and capital budgeting.

What Decision Makers Actually Use

Across multiple audits, the most frequently used sections are:

Executive summary

Opportunity register

Capital staging plan

Financial summary table

Detailed appendices are important for engineering validation.

But decisions are made from structured, commercial clarity.

If you are reviewing an energy audit provider, ask to see a de-identified sample report. You should be able to quickly identify:

Clear baseline

Clear savings register

Clear capital requirement

Clear prioritisation

Clear financial treatment

If it reads like a technical thesis, it will not drive action.

If you want to understand the broader scope of commercial and industrial energy audits in Australia, this guide explains what is included and how they are structured.

For details on audit levels under AS/NZS 3598, see our breakdown of Type 1, Type 2, and Type 3 energy audits.

If you want a clearer view of deliverables, see what you receive from a commercial energy audit and how reports are structured for decision-making.

Next Step

We can review your energy spend, site constraints, and budget cycle to determine whether a Type 2 or Type 3 audit is appropriate. We are also avavible If you would like to see what a decision-ready energy audit report for your site would look like

The goal is simple.

Give you a report that supports real operational and capital decisions.

Find out about available energy reduction grants and subsidies for your organisation on our Grants page.